Open uping the Potential of ADUs Through Financial Support

For homeowners looking for ADU funding grants in 2025, here are the key programs currently available:

| State/City | Grant Amount | Key Requirements |

|---|---|---|

| California | Up to $40,000 | Income below 80% AMI, owner-occupied property |

| Vermont | Up to $50,000 | Must rent at/below market rates for 5+ years |

| New York | Up to $125,000 | Part of $85M allocation over 5 years |

| Los Angeles County | Up to $75,000 | Forgivable loan format |

| Santa Cruz | Up to $40,000 | Includes fee waivers/reductions |

The housing crisis in California and across the United States has prompted innovative solutions, with ADU funding grants emerging as a powerful tool to expand affordable housing options. Accessory Dwelling Units (ADUs) – whether they’re converted garages, basement apartments, or newly constructed backyard cottages – offer a practical way to increase housing density while providing homeowners with rental income or space for family members.

As one program administrator noted: “California homeowners, the state wants to pay you $40,000 to build an accessory dwelling unit with this CalHFA ADU grant!”

These grants are designed to overcome one of the biggest problems in ADU construction: the upfront costs. Pre-development expenses like architectural designs, permits, and impact fees can quickly add up to tens of thousands of dollars before construction even begins. Government agencies have recognized this barrier and created dedicated funding programs to help homeowners take the first steps.

The benefits extend beyond individual homeowners. Communities gain additional housing units without major infrastructure changes, local economies benefit from construction activity, and more affordable housing options become available in established neighborhoods.

Why this matters: In 2025, housing production continues to lag behind market demand in many regions, leading to skyrocketing prices and extended commute times. ADUs represent a relatively quick and less disruptive way to add housing stock to existing neighborhoods.

If you’re considering building an ADU, exploring available grant programs should be your first step before committing to more traditional financing options.

Understanding ADU Funding Grants

What Are ADU Funding Grants?

ADU funding grants are a homeowner’s dream come true – financial assistance that doesn’t need to be paid back, specifically designed to help you build that backyard cottage or garage apartment you’ve been thinking about. These grants come from government agencies and non-profit organizations that recognize the critical role ADUs play in addressing our housing shortage.

Unlike traditional loans that follow you for years, these grants are gifts with a purpose: creating more affordable housing options in neighborhoods where people already want to live. As housing prices continue to climb and commutes get longer, ADUs offer a practical solution that works for everyone.

I love how one California program administrator put it: “The state wants to pay you $40,000 to build an accessory dwelling unit!” That’s a pretty compelling invitation to join the housing solution, isn’t it?

These grants are particularly valuable for low and moderate-income homeowners who might otherwise find it impossible to come up with the substantial upfront costs of ADU development. By removing this financial barrier, more diverse homeowners can participate in creating housing solutions while potentially generating rental income for themselves.

Types of Costs Covered by ADU Grants

When you receive an ADU funding grant, it’s important to understand what it will – and won’t – cover. Most grants focus on getting you through the expensive pre-development phase rather than funding the entire construction project.

Think of these grants as covering everything you need before you hammer the first nail. This typically includes architectural designs that bring your vision to life, permitting fees that can otherwise cause sticker shock, and site preparation to get your property ready for construction.

Many homeowners are surprised by how expensive the paperwork phase can be. Between impact fees charged by local governments, necessary feasibility studies to determine if your property can support an ADU, and soil tests to ensure proper foundation design, costs add up quickly.

Your grant might also cover property surveys to precisely measure boundaries and energy reports that evaluate efficiency requirements. These technical necessities often cost thousands of dollars before construction even begins.

It’s worth noting what these grants typically don’t cover – as one California administrator clarified: “The grant does not cover most hard construction costs such as foundation work, framing, interior finishes, labor, materials, and solar installations.” Once your plans are approved, you’ll likely need construction financing for the building phase itself.

Eligibility Requirements for ADU Grants

Before you get too excited about ADU funding grants, let’s talk about whether you qualify. While requirements vary between programs, most share common eligibility criteria that help target the assistance to those who need it most.

Income limits are the first hurdle for most programs. If you’re in California, you’ll typically need to earn below 80% of your county’s Area Median Income. This varies dramatically by location – in Los Angeles County, that’s around $84,160 for a family, while in pricier Marin County, you might qualify with income approaching $300,000 due to the higher cost of living.

Almost every program requires owner-occupancy – the property must be your primary residence, not an investment property. This ensures the grants benefit actual homeowners rather than developers looking to maximize profits.

Your property itself needs to meet certain criteria too. It must be located within the jurisdiction offering the grant (usually your city or county), typically be a single-family home or small multi-unit building with 1-4 units, comply with local zoning laws, and be free from certain legal issues.

Some programs also care about how you’ll use the ADU after it’s built. Vermont’s program, for example, requires that you rent your ADU at or below market rates for at least 5 years. Many programs explicitly prohibit using your grant-funded ADU as a short-term vacation rental.

Timing matters too – you generally can’t get reimbursed for an ADU you’ve already completed. As one program explains in their FAQ: “Applicants must be in the process of construction without having already received a Certificate of Occupancy for the ADU.”

Be prepared for paperwork! You’ll need to document everything from your income (tax returns, pay stubs) to property ownership, utility bills, mortgage details, and detailed project plans. The documentation requirements can be substantial, but the potential financial benefit makes the effort worthwhile.

According to research by AARP, these grant programs are making a meaningful difference in expanding housing options while helping homeowners build equity. With housing shortages affecting communities nationwide, ADU funding grants represent a smart investment in sustainable community development.

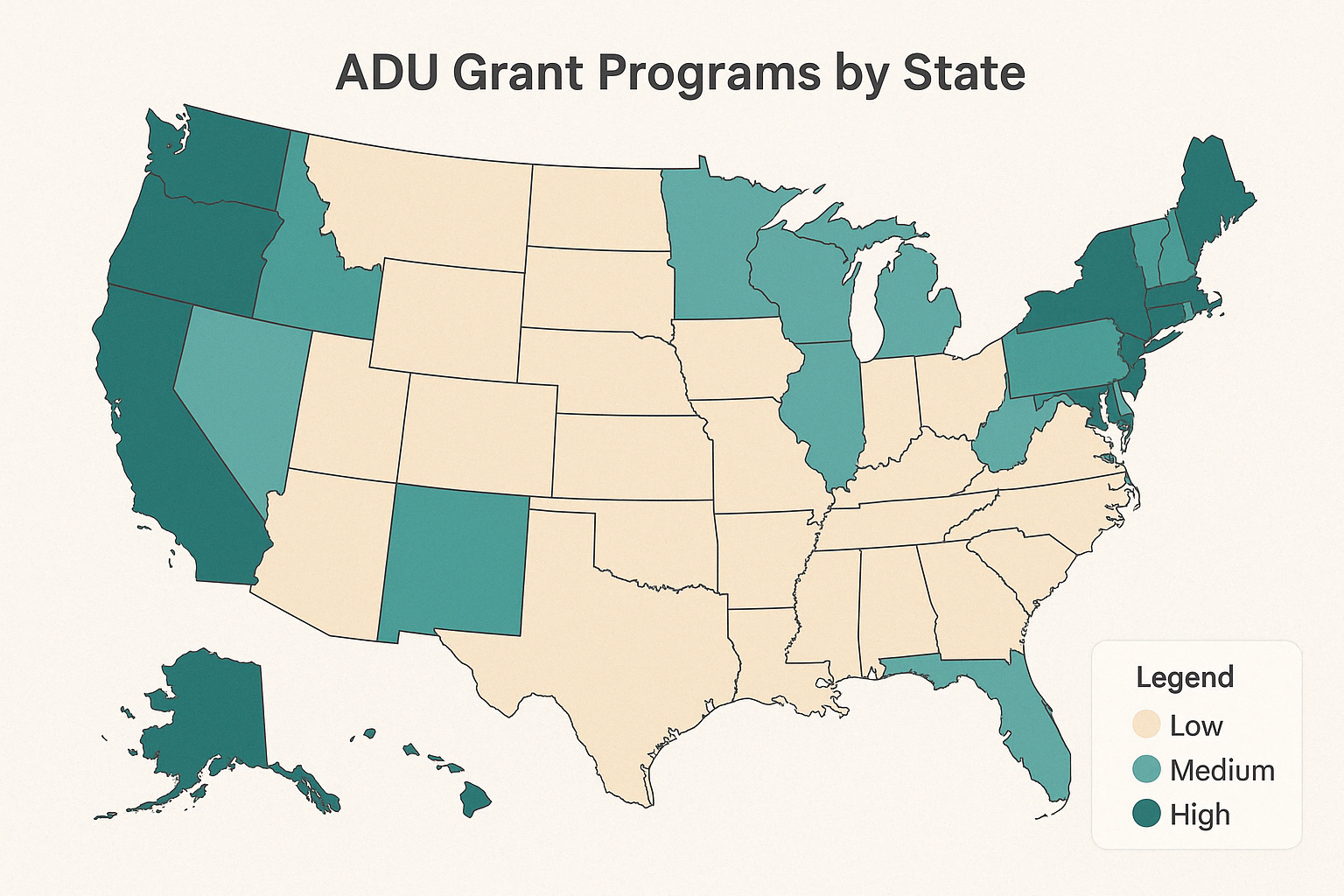

State and City-Specific ADU Grant Programs

The availability of ADU funding grants varies significantly by location, with some states and cities offering more generous programs than others. Here’s a detailed look at some of the most notable programs across the United States in 2025:

California’s ADU Grant Program

California leads the nation in ADU policy innovation and funding support, which makes perfect sense given the state’s housing crunch. If you’re a California homeowner, you’re in luck! The California Housing Finance Agency (CalHFA) offers one of the most substantial grant programs in the country.

How substantial? We’re talking up to $40,000 to help get your ADU project off the ground. That’s nothing to sneeze at!

The CalHFA ADU Grant Program launched in 2021 with an impressive $100 million allocation. It proved so popular that they added a second phase in 2023-2024 with an additional $25 million in funding. For 2025, the program continues to target those pre-development costs that often stop homeowners in their tracks – things like architectural plans, permits, and other upfront expenses.

One thing I love about this program: it’s genuinely free money. As one program administrator put it: “Yes, the ADU grant provided by CalHFA is free and does not need to be repaid. However, recipients will receive a 1099 form for the tax year in which the grant funds were disbursed.” (So do keep tax implications in mind!)

To qualify, you’ll need to have an income below 80% of your county’s Area Median Income. You must live in the property where you’re building the ADU, and it needs to be your primary residence – not an investment property. The program works with single-family homes or 2-4 unit buildings.

The application process is straightforward but requires working with an approved lender. You’ll need to secure a construction loan, complete the grant application with all required documentation, and then you can begin the pre-development phase once prequalified. The grant funds come through a managed escrow account.

One word of caution: these grants go fast! The funding round that opened in late 2024 was fully allocated within weeks – serving about 600 homeowners. If you’re interested in applying in 2025, you’ll want to be ready to pounce when the next round opens.

Vermont’s Housing Improvement Program

Vermont takes a different approach with its Housing Improvement Program, administered by the Vermont Housing & Conservation Board (VHCB). And it’s a generous one!

This program offers up to $50,000 per unit and focuses on creating affordable rental housing, including ADUs. What makes Vermont’s program unique is its emphasis on long-term community benefit.

To qualify, property owners must agree to rent the ADU at or below market rates for at least 5 years. They also give priority to projects that will house individuals exiting homelessness – a wonderful way to address multiple community needs at once.

As one housing advocate quipped: “And you thought Montpelier was all about the maple syrup.” The state has shown remarkable innovation in addressing housing shortages through ADU development. It’s a testament to Vermont’s community-minded approach to housing solutions.

The program also requires that your property meets all local building and zoning requirements – which is standard for pretty much any grant program you’ll encounter.

New York’s Plus One ADU Program

New York State has created an ambitious program that might make other states a bit jealous. Their Plus One ADU Program offers grants of up to $125,000 – significantly more than most other programs nationwide.

The state has allocated $85 million over five years as part of New York’s broader housing plan, with funding continuing through 2025. What distinguishes this program is its comprehensive approach, potentially covering not just pre-development but construction costs as well.

Like most programs, New York focuses on low- and middle-income homeowners with owner-occupied properties. Your ADU must comply with local zoning and building codes (as always).

What’s interesting about New York’s approach is that unlike California’s direct-to-homeowner method, New York’s program first provides funding to local entities (municipalities and non-profits), which then distribute grants to eligible homeowners. This creates a more localized system of support.

The program takes a full-service approach, supporting homeowners throughout the entire ADU journey – from pre-development (design, budgeting, permitting) through construction oversight (contractor selection, compliance monitoring) and even post-construction monitoring (regulatory agreements, compliance certifications).

Other Notable City Programs

Several cities have created their own ADU funding grants and incentives that are worth exploring if you live in these areas:

Los Angeles County offers the Second Dwelling Unit Pilot Program with subsidies of up to $75,000 per ADU in the form of a forgivable loan. That’s a significant amount that can make a real difference in your project’s feasibility.

Santa Cruz County provides forgivable loans of up to $40,000 and sweetens the deal by waiving or reducing permitting fees for ADU construction – addressing both upfront costs and ongoing expenses.

Portland homeowners can save up to $15,000 through development fee waivers for ADUs, making the city one of the most ADU-friendly in the nation.

Boston offers deferred equity loans of up to $30,000 for ADU construction, providing another flexible financing option for homeowners.

Austin’s Alley Flat Initiative provides fee waivers and expedited permitting for ADUs that meet affordability requirements – helping projects move forward faster while encouraging affordable housing solutions.

As one housing advocate aptly put it: “Programs incentivizing accessory dwelling units are popping up from coast to coast, as local governments and coalitions seek real solutions to housing shortages.”

The landscape of ADU funding is constantly evolving, with new programs emerging regularly in 2025. If you don’t see your location listed here, it’s worth checking with your local housing authority or planning department – you might be pleasantly surprised by what’s available in your area!

How to Apply for ADU Funding Grants

Navigating the application process for ADU funding grants might seem daunting at first, but with the right preparation, you can significantly improve your chances of success. I’ve helped many homeowners through this journey, and I’m excited to share what I’ve learned along the way.

Gathering Necessary Documentation

Before you dive into any application forms, take some time to collect all your paperwork. Think of this as creating your “ADU grant toolkit” – having everything organized from the start will save you countless headaches later.

Most grant programs will ask for proof of your income situation. This typically includes your recent pay stubs (usually the last 2-3 months), bank statements showing your financial stability, and tax returns from the past couple of years. If you’re self-employed, be prepared to provide additional documentation about your business income.

Your property paperwork is equally important. You’ll need your deed, recent mortgage statements, and property tax records to prove ownership. Got your property in a trust? No problem – just include trust documentation showing you’re either a trustee or beneficiary.

Project plans are another crucial element. Most grant administrators want to see that you’ve thought through your ADU project carefully. Have your architectural drawings ready, along with contractor bids and detailed cost estimates. A realistic project timeline also shows you’ve done your homework.

Don’t forget the basics – your government-issued ID, Social Security number, and current contact information. You’ll also need to provide property details like your address, recent utility bills, and mortgage information.

As one program administrator candidly told me: “Having a completed application does not guarantee you will receive a grant.” This honest assessment highlights why being thorough with your documentation matters so much.

Working with Approved Lenders

Most ADU funding grant programs don’t operate in isolation – they’re typically connected to construction financing options. This is especially true in California, where the process often starts with finding the right lender.

Start by reviewing the list of participating lenders provided by your grant program. Each lender might have slightly different requirements, so it’s worth calling a few to find the best fit for your situation. Some are more experienced with ADU projects than others, which can make a big difference in how smoothly the process goes.

Before you can formally apply for most grants, you’ll need to secure pre-approval for a construction or renovation loan. This step shows the grant administrator that you have a viable plan for completing the entire project, not just the pre-development phase.

Understanding the escrow process is another key aspect of working with lenders on grant-funded projects. Rather than handing you a check, most programs disburse funds into a managed escrow account. From there, payments go directly to your vendors – architects, permit offices, and contractors – as you reach various project milestones.

Here’s some good news that many homeowners don’t realize: “Rental income from a proposed ADU can now—finally!—be counted toward your qualifying income for an ADU loan.” This policy change has opened doors for many homeowners who previously couldn’t qualify for the necessary construction financing.

For more details about financing options, you might find our guide to ADU Loan Rates helpful as you evaluate different lenders.

Step-by-Step Application Process

Let me walk you through what the typical application journey looks like for ADU funding grants in 2025:

The process begins with thorough research and preparation. Take time to determine your eligibility based on the specific program requirements and gather all necessary documentation. This upfront investment of time will pay dividends later.

Next comes lender selection – choose an approved lender from the program’s list and begin the loan pre-approval process. Your lender will become an important partner in this journey, so select someone who communicates clearly and has experience with ADU projects.

When you’re ready to submit your grant application, your lender will typically assist you with completing the forms and ensuring all required documentation is included. Their expertise can help you avoid common pitfalls that might delay your application.

Once submitted, your application enters the review phase, where the grant administrator verifies your eligibility and ensures your application is complete. This might take anywhere from a few weeks to a couple of months, depending on the program.

If approved, you’ll receive notification that funds have been reserved specifically for your project – a moment worth celebrating! Now you can confidently begin the pre-development phase, working with architects, engineers, and local permitting offices, with costs covered by the grant.

As your project progresses, grant funds are typically disbursed directly to service providers through the escrow account, simplifying the payment process. Once pre-development is complete, your construction loan kicks in to fund the actual building of your ADU.

One important tip I can’t stress enough: many programs operate on a first-come, first-served basis, and funding rounds can be depleted incredibly quickly. As one program update recently noted: “The ADU grant allocation in California was exhausted within weeks at the start of 2025.” This underscores the importance of having your application ready to submit as soon as a new funding round opens.

The application process might seem complex, but each step brings you closer to making your ADU dream a reality while leveraging valuable financial support through ADU funding grants.

Alternative Financing Options If Grants Are Unavailable

When you’ve set your heart on building that perfect ADU but find that ADU funding grants are either unavailable or won’t cover enough of your costs, don’t worry – you still have plenty of options. Let’s explore some alternative financing routes that might work for your situation.

Home Equity Loans and HELOCs

If you’ve built up equity in your home over the years, you might be sitting on an untapped resource for your ADU project. Home equity loans give you a lump sum with a fixed interest rate, while Home Equity Lines of Credit (HELOCs) work more like a credit card you can draw from as needed.

The beauty of these options is their flexibility – you can use the funds however you want without the restrictions that often come with grants. Plus, the interest might be tax-deductible (though you’ll want to check with your tax advisor on that).

But there’s a catch – you need substantial equity in your home to make this work. One financing expert I spoke with put it plainly: “A home valued at $500,000 with an outstanding mortgage of $400,000 might offer $0 borrowing power with a traditional home equity loan due to 80% LTV restrictions.” In other words, if you’re still paying off most of your mortgage, this might not be your best bet.

And remember, these loans use your home as collateral. If things go sideways financially, your primary residence could be at risk.

Renovation Loans

Now here’s an interesting option that’s gaining traction – renovation loans based on what your property will be worth after the ADU is built.

Unlike traditional loans that only look at your current home value, renovation loans consider the “after-renovation value,” which can dramatically increase your borrowing power. One lender explained it this way: “While traditional home equity loans may offer $0 borrowing power due to an 80% LTV, an alternative financing option can allow borrowing up to $176,000 by using the anticipated after renovation value.”

These loans do require more paperwork and planning – you’ll likely need detailed project plans and contractor quotes – but for many homeowners, the extra effort open ups funding that would otherwise be unavailable.

Construction Loans

If you’re building a brand-new ADU from the ground up, construction loans are worth considering. These short-term loans are specifically designed for building projects, with funds released in stages as construction progresses.

One nice feature of many construction loans is that they can convert to a permanent mortgage once your ADU is complete, saving you the hassle of refinancing. However, be prepared for higher interest rates than traditional mortgages and a more rigorous approval process. Lenders want to see detailed plans, budgets, and often require working with approved contractors.

Cash-Out Refinancing

With cash-out refinancing, you replace your existing mortgage with a new, larger one and pocket the difference in cash. This option often offers the lowest interest rates among financing alternatives, which makes it attractive for larger ADU projects.

But timing matters enormously with this option. As one financial advisor cautioned me, “Refinancing can jeopardize favorable mortgage rates.” If you locked in a great rate a few years ago, replacing it with today’s higher rates might not make financial sense, even with the cash you’d get for your ADU.

Also keep in mind that refinancing comes with closing costs and resets your mortgage term – potentially adding years to your loan.

Specialized ADU Loan Programs

The growing popularity of ADUs has led some lenders to create financing products specifically for these projects. These specialized loans are designed with the unique aspects of ADU construction in mind and sometimes include helpful features like project management support.

One option worth mentioning is the CalCon Mortgage Loan, which allows homeowners to take out a second position loan (typically with interest rates between 6-8%) without refinancing their primary mortgage. This can be a lifesaver if you want to maintain your existing mortgage rate.

| Financing Option | Typical Interest Rates | Loan Amounts | Best For |

|---|---|---|---|

| Home Equity Loan | 6-8% | Up to 80-85% of home equity | Homeowners with significant equity |

| HELOC | 7-10% (variable) | Up to 85% of home equity | Flexible funding needs |

| Renovation Loan | 6-9% | Based on after-renovation value | Maximizing borrowing power |

| Construction Loan | 7-12% | Based on project cost | New construction projects |

| Cash-Out Refinance | 6-8% | Up to 80% of home value | Those with favorable refinancing conditions |

| Specialized ADU Loans | 6-8% | $200,000+ | Those who don’t want to refinance primary mortgage |

When ADU funding grants aren’t available, taking the time to explore these financing alternatives can make the difference between shelving your ADU dreams and breaking ground on your project. Each option has its strengths and limitations, so consider consulting with a financial advisor who can help you choose the best path based on your specific situation and goals.

For more detailed information about loan options, you might find our guide to ADU Financing Options helpful, along with current information about ADU Loan Rates.

Maximizing the Impact of ADU Grants on Affordable Housing

When we talk about ADU funding grants, we’re not just discussing a financial boost for individual homeowners. These grants are powerful tools that ripple through communities, creating lasting positive change in our neighborhoods and addressing crucial housing needs.

Creating Affordable Housing Options

The housing crisis affects communities across America, with many families struggling to find affordable places to live. This is where ADUs shine brightest.

ADU funding grants help create what urban planners call “gentle density” – adding homes without dramatically changing neighborhood character. Unlike massive apartment complexes that can transform an area overnight, ADUs blend seamlessly into existing communities while providing much-needed housing options.

What makes ADUs special is their natural affordability. Since they’re typically smaller than traditional homes (usually between 400-1,200 square feet), they cost less to build and rent, making them accessible to more people even without formal rent restrictions. A backyard cottage or converted garage might rent for 20-30% less than a comparable apartment in the same neighborhood.

These units also foster multi-generational living arrangements that benefit families financially and emotionally. I recently spoke with a homeowner in Portland who built an ADU for her aging mother, allowing her to live independently while remaining close enough for regular family dinners and emergency support. “It’s given Mom her dignity and us peace of mind,” she explained. “The grant made it possible when we couldn’t have afforded it otherwise.”

Community Development Benefits

The positive effects of ADU funding grants extend far beyond individual properties, creating a ripple effect throughout neighborhoods and local economies.

When a homeowner builds an ADU, they’re not just creating housing – they’re generating jobs. From architects and contractors to plumbers and electricians, each project supports multiple local businesses. One economic study estimated that every ADU construction project supports approximately 1.5 local jobs and generates thousands in economic activity that stays within the community.

Well-designed ADUs can also boost property values throughout a neighborhood. Rather than diminishing home values (as some initially feared), tastefully constructed ADUs often improve curb appeal and make neighborhoods more desirable. They represent an investment in the community’s future.

What’s particularly smart about ADU development is how efficiently it uses existing infrastructure. Unlike new subdivisions that require new roads, sewers, and utility lines, ADUs tap into systems already in place. This makes them environmentally friendly too – studies show that infill development like ADUs produces significantly lower carbon emissions than equivalent housing in new suburban developments.

Many grant programs are specifically designed to benefit communities that have historically lacked investment. California’s program, for instance, directs 42% of its funds toward socially disadvantaged areas, supporting Black, Indigenous, and People of Color communities that have often been excluded from housing assistance in the past.

Tax Implications of Receiving ADU Grants

While ADU funding grants offer tremendous benefits, it’s important to understand their tax implications before diving in.

Most grant recipients are surprised to learn that grant money is typically considered taxable income. As one California program administrator plainly states: “Yes, the ADU grant is free money, you do not have to pay it back. However, you will receive a 1099 for the following tax year.” This means you’ll need to report that money on your tax return and potentially pay taxes on it.

The silver lining? Many costs associated with ADU construction may be tax-deductible, especially if you plan to use the unit as a rental property. This can help offset the tax impact of receiving the grant. Common deductions include property taxes, mortgage interest, insurance, maintenance costs, and depreciation.

If you do rent out your ADU, you’ll need to report that rental income on your taxes. However, the IRS allows you to deduct many expenses associated with being a landlord, which can significantly reduce your tax liability. Some homeowners find that the long-term tax benefits of having a rental property actually outweigh the one-time tax hit from receiving the grant.

It’s also worth noting that adding an ADU will likely increase your property’s assessed value, which means your property taxes may go up. The increase varies widely by location – some areas offer temporary property tax breaks for ADUs, while others assess them at full value immediately.

Given all these variables, I strongly recommend consulting with a tax professional familiar with real estate investments before applying for an ADU funding grant. A good accountant can help you understand exactly how a grant will affect your specific financial situation and develop strategies to minimize any negative tax impacts.

The tax considerations might seem daunting, but for most homeowners, they’re a small price to pay for the substantial benefits an ADU brings – both to your property value and to your community’s housing needs.

Frequently Asked Questions about ADU Funding Grants

Are ADU grants considered taxable income?

Yes, those ADU funding grants you’ve been eyeing do typically count as taxable income. When you receive grant funds, the program will send you a 1099 form for that tax year, which means Uncle Sam will want his share.

I remember talking with a homeowner in San Diego who was surprised by this. “I thought it was free money,” she told me. “It is free in the sense you don’t repay it, but the IRS still considers it income.”

The good news? The tax implications might not be as scary as they sound. Many expenses related to your ADU project could potentially offset the tax impact through deductions. A savvy tax professional who understands real estate can help you steer this landscape and possibly minimize your tax burden. Each situation is unique, so personal tax advice is definitely worth the investment here.

Can I get reimbursed for expenses already paid?

Unfortunately, most ADU funding grants won’t cover expenses you’ve already paid out-of-pocket. These programs are typically designed to pay for upcoming costs, not reimburse you for that architect you already hired or those permit fees you already covered.

As one California homeowner finded: “I had already paid for my architectural plans when I learned about the grant. The program administrator explained they couldn’t reimburse me directly, but they could help in another way.”

That “other way” is important to understand. While direct reimbursement is usually off the table, some programs allow those receipts to reduce your construction loan principal if financed appropriately. It’s not cash back in your pocket, but it could mean a smaller loan balance in the long run. Think of it as getting credit for your initiative rather than a refund.

What are the limitations on renting out my ADU?

When it comes to renting your newly built ADU, the strings attached to your ADU funding grants vary considerably depending on the program. Understanding these limitations before you apply is crucial.

In Vermont, for instance, their Housing Improvement Program requires you to rent at or below market rates for at least five years. “We were fine with this restriction,” shared one Vermont homeowner. “We wanted to provide affordable housing for a local teacher anyway, so it aligned with our goals.”

Many programs explicitly prohibit short-term rentals like Airbnb or VRBO. This makes sense when you consider these grants aim to increase long-term housing stock, not vacation rentals.

Some of the more structured programs might require you to verify your tenants’ income levels or sign a regulatory agreement that spells out your obligations for 5-10 years. These agreements become part of your property record, so they’re not something to take lightly.

Before you commit to any grant program, carefully review the rental restrictions to ensure they align with your long-term plans for the ADU.

Can I apply for a grant if my property is in a trust or LLC?

Trust structures are generally okay for ADU funding grants, but LLCs are typically a no-go. If your home is in a family trust, you’ll need to prove you’re either a trustee or beneficiary and that you actually live in the home as your primary residence.

“When I applied, I worried my family trust would disqualify me,” shared a homeowner from Santa Cruz. “But the program administrator walked me through the additional documentation needed, and everything worked out fine.”

Properties held in LLCs, however, usually don’t qualify for these grants. The programs are designed to help individual homeowners, not business entities. If your property is currently in an LLC structure, you might need to consider restructuring ownership before applying.

What happens if I don’t use all of the grant funds?

Here’s some good news—leftover ADU funding grants don’t disappear into thin air. If your pre-development costs come in under budget, those remaining funds typically stay in the escrow account established for your project.

Most programs allow these unused funds to reduce your construction loan principal or even buy down your interest rate. One California homeowner told me, “My permits cost less than expected, and I was thrilled to learn the remaining $3,200 could go straight toward reducing my loan balance.”

This flexibility is a nice feature of these programs, ensuring that every dollar allocated to your project ultimately benefits you, even if your initial cost estimates were a bit high.

Can I apply for grants for multiple properties?

If you’re hoping to build ADUs on multiple properties using these grants, I have disappointing news. Most ADU funding grants limit eligibility to your primary residence only. These programs are designed specifically to help homeowners, not investors or developers building multiple units across different properties.

“I own my home plus a rental property next door,” explained one homeowner. “The program administrator was very clear that only my primary residence qualified for the grant.”

This restriction serves an important purpose—it ensures the limited grant funds help as many individual homeowners as possible rather than concentrating benefits with those who own multiple properties. The focus remains on creating more housing where homeowners actually live, contributing to community stability while increasing housing options.

If you own multiple properties and want to build ADUs on each, you’ll likely need to explore alternative financing options for any properties beyond your primary residence.

Conclusion

ADU funding grants have opened doors for countless homeowners who might otherwise find building an accessory dwelling unit financially out of reach. From California’s generous $40,000 program to Vermont’s $50,000 offering and New York’s impressive $125,000 allocation, these grants are making dreams of extra living space a reality for people from all walks of life in 2025.

But the beauty of these programs goes well beyond the individual homeowner’s bank account. When you build an ADU, you’re actually contributing to the bigger picture. Your neighborhood gains a much-needed affordable housing unit. Families find flexible living arrangements that keep generations connected. And communities grow organically without losing their unique character or requiring massive infrastructure overhauls.

As I’ve talked with homeowners who’ve successfully steerd the grant process, one thing becomes clear: planning ahead makes all the difference. If you’re considering taking the plunge into ADU ownership, here’s what I recommend:

First, do your homework on local programs. Grant availability changes frequently—sometimes funding rounds close within days of opening—so connect with your local housing agencies for the most up-to-date information. What was available last month might not be there today, and new opportunities emerge regularly.

Second, think beyond just the grant itself. Most grants cover pre-development costs but not actual construction. Have a comprehensive financial plan that addresses both phases of your project. That might mean exploring some of the alternative financing options we discussed earlier.

Third, get your paperwork in order before you apply. The difference between success and disappointment often comes down to documentation. Have your income verification, property records, and project plans ready to go, and consider working with professionals who’ve been through the process before.

Finally, don’t put all your eggs in the grant basket. If programs in your area are limited or highly competitive, remember there’s more than one path to ADU ownership. Home equity loans, renovation financing, and specialized ADU lending products can all help make your project viable.

At ADU Marketing Pros, we’ve watched the ADU landscape evolve dramatically across California’s major markets. While our specialty is helping ADU builders and architects connect with homeowners like you, we’ve developed a deep understanding of what makes these projects succeed from start to finish.

The journey to creating your ADU might seem daunting at first glance—a maze of applications, regulations, and financing options. But remember that each successful project brings us one step closer to addressing the housing challenges facing our communities. Your backyard cottage or converted garage isn’t just an investment in your property; it’s an investment in the future of your neighborhood.

With the right information and support, your ADU dream is well within reach. And when that day comes when you’re standing in your completed accessory dwelling unit—whether it’s welcoming a parent, housing a young adult, or greeting a new tenant—you’ll understand why so many homeowners call their ADU project one of the best decisions they ever made.