Construction loans for adu are a crucial topic for homeowners looking to maximize property value and generate rental income. If you’re exploring options for an accessory dwelling unit in urban California, here’s a quick overview:

- Definition: ADUs, or Accessory Dwelling Units, are secondary residential spaces on the same lot as a primary residence.

- Value: ADUs provide flexibility. They can serve as rental units, housing for family members, or guest accommodations.

- Demand: The appeal of an ADU has risen significantly. This trend is fueled by regulatory shifts and a growing need for affordable housing.

ADUs, often called granny flats or in-law suites, have transformed from mere auxiliary structures into valuable assets on a property. They offer independence for families and supplement income streams, all while increasing overall property value.

The current surge in ADU demand is particularly notable in California’s urban and suburban areas. Changes in zoning laws have eased construction restrictions, making it simpler than ever to build these units. Municipalities are not only permitting but actively encouraging ADUs as they tackle housing shortages and aim to boost neighborhood density.

As people seek efficient ways to achieve financial and living flexibility, understanding construction loans becomes crucial. These loans can support the high costs of establishing an ADU, which often range from $100,000 to $300,000. Securing appropriate financing allows homeowners or firms to make informed decisions, optimizing both their project plans and long-term financial benefits.

By focusing on clear and strategic financing, businesses and homeowners can grasp the full potential of ADUs, turning these secondary havens into prime investments.

Construction loans for adu definitions:

– adu financing options

– adu loan rates

Understanding Construction Loans for ADUs

When you’re considering building an ADU, understanding your loan options is crucial. The right financing can make or break your project. Let’s explore the different types of loans available for ADUs and what they mean for you.

Home Equity Line of Credit (HELOC)

A HELOC is like a credit card for your home. You borrow against the equity you’ve built up. It’s flexible because you can withdraw money as you need it, which is great for a project with unpredictable costs.

Benefits of HELOC:

– Flexibility: Borrow only what you need, when you need it.

– No need to refinance: Keep your existing mortgage rate if it’s low.

Drawbacks of HELOC:

– Variable interest rates: Your payments could increase if rates rise.

– Limited borrowing power: Often capped at 80% of your home’s current value.

Home Equity Loan

A Home Equity Loan is a bit different. You get all the money upfront and pay it back over time with fixed monthly payments. It’s a good choice if you want to lock in today’s interest rates.

- Fixed-rate loans: Your interest rate stays the same, providing payment stability.

- Borrowing full balance: Receive a lump sum to cover your ADU costs.

Cash-out Refinance

Refinancing your mortgage can also provide funds for an ADU. This involves replacing your existing mortgage with a new one, ideally at a lower rate, and taking out extra money based on your home’s equity.

- Accessing home equity: Use the increased value of your home to fund your ADU.

- Potentially larger loan: Borrow more than with a HELOC or Home Equity Loan, especially if your home value has increased.

Each of these options has its pros and cons. The best choice depends on your financial situation, interest rates, and how much equity you have in your home. Understanding these options helps you make a smart decision for financing your ADU project.

Factors Influencing ADU Loan Eligibility

When you’re planning to finance an ADU, understanding the factors that influence loan eligibility is crucial. These factors help lenders determine your ability to repay the loan and the level of risk involved. Let’s explore the key factors: credit score, loan-to-value (LTV) ratio, and debt-to-income (DTI) ratio.

Credit Score

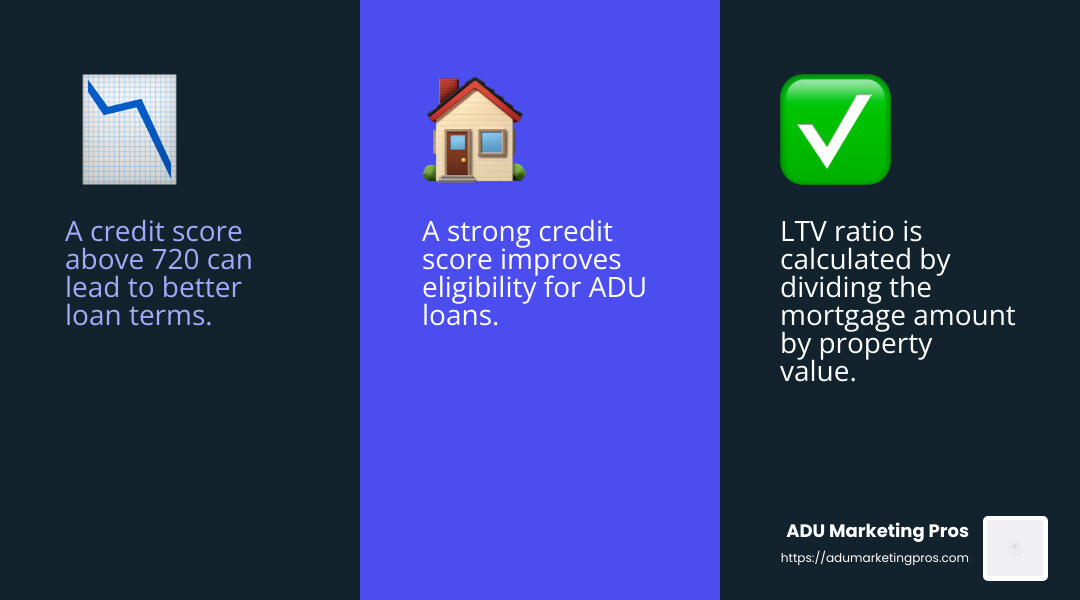

Your credit score is a numerical representation of your creditworthiness. It reflects how reliably you’ve paid debts in the past. A higher credit score can qualify you for better loan terms and lower interest rates.

- Credit Score Importance: Scores above 720 are considered very strong, making you eligible for more favorable loan conditions.

Loan-to-Value (LTV) Ratio

The LTV ratio is a measure of the loan amount relative to the appraised value of your property. It’s calculated by dividing the total mortgage amount by the property’s current market value.

-

LTV Calculation: For example, if your home is worth $1,000,000 and you have a $550,000 mortgage, your LTV is 55%.

-

LTV Importance: A lower LTV ratio indicates less risk for lenders, as it shows more equity in your home. Most banks prefer an LTV of 80% or less for ADU loans.

Debt-to-Income (DTI) Ratio

The DTI ratio compares your monthly debt payments to your monthly income. It helps lenders assess your ability to manage additional debt.

-

DTI Calculation: Add up all your monthly debt obligations (like mortgage, car loans, credit card payments) and divide by your gross monthly income.

-

DTI Importance: Banks typically prefer a DTI of 40-45%. A lower DTI means you have more income available to handle new loan payments, making you a safer bet for lenders.

Understanding these factors helps you better prepare for the loan application process. By knowing your credit score, LTV, and DTI, you can make informed decisions and improve your chances of securing the right construction loan for ADU projects.

Next, we’ll steer the ADU loan process, covering application steps, lender selection, and the essential documentation you’ll need.

Navigating the ADU Loan Process

When you’re ready to finance your ADU, navigating the loan process can feel overwhelming. But don’t worry. We’ll break it down into simple steps.

Assessing Personal Financial Situation

Before diving into loan applications, it’s important to assess your financial situation. This means understanding your home’s value, your income, and your current debts.

-

Estimate Home Value: Knowing the current market value of your home is crucial. You can do this by getting a professional appraisal or using online tools. This helps determine your loan-to-value (LTV) ratio, which is key for lenders.

-

Review Income and Debts: Calculate your monthly income and total debts. This will help you understand your debt-to-income (DTI) ratio. Lenders use this ratio to assess your ability to manage new debt.

-

Check Credit Score: A strong credit score can open doors to better loan terms. Aim for a score above 720 to qualify for favorable conditions.

Gathering Necessary Documentation

Once you’ve assessed your finances, it’s time to gather the necessary documents. Lenders will need these to verify your information and assess your loan eligibility.

Here’s what you’ll typically need:

-

Pay Stubs: Provide your two most recent pay stubs to show your current income.

-

W-2 Forms: Lenders will want to see your W-2 forms from the past two years. These verify your employment and income history.

-

Mortgage Statements: Your most recent mortgage statement helps lenders understand your current loan obligations.

-

Bank Statements: Provide statements for personal bank accounts, retirement accounts, and any investment accounts. These demonstrate your financial stability.

-

Homeowners Insurance Proof: This shows that your property is insured, which is a requirement for most loans.

-

Contractor Information and Renovation Plans: If you have already selected a contractor, include their information and detailed renovation plans. This helps lenders understand the scope and cost of your ADU project.

Loan Application Steps

-

Research Lenders: Not all lenders offer the same terms. It’s wise to shop around and get quotes from multiple lenders. Look for those with experience in construction loans for ADUs.

-

Pre-Qualification: Use tools like the RenoFi Self Pre-Qualification tool to see if you’re a good fit for specific loans. This step gives you a ballpark idea of how much you can borrow.

-

Submit Application: Once you’ve selected a lender, fill out their application form. Be prepared to answer questions about your finances and the ADU project.

-

Verification and Approval: After submission, the lender will verify your documents. They might ask for additional information, so respond promptly to keep the process moving.

-

Loan Approval: If everything checks out, you’ll receive a loan offer. Review the terms carefully before accepting.

Navigating the ADU loan process involves careful planning and preparation. By understanding your financial situation and gathering the right documents, you can confidently approach lenders and secure the financing you need for your ADU project.

Next, we’ll address some frequently asked questions about construction loans for ADUs, including interest rates and down payment requirements.

Frequently Asked Questions about Construction Loans for ADUs

Can you get a construction loan for an ADU?

Yes, you can get a construction loan for an ADU, but there are limitations. Construction loans are designed to finance the building of structures from the ground up. They often come with higher interest rates and strict requirements. Lenders typically require a detailed plan and budget, and they may ask for a draw schedule from your contractor.

However, construction loans aren’t always the best option for ADUs. They can be complex and involve higher closing costs. Alternatives like Home Equity Lines of Credit (HELOCs) might be more suitable. These options can offer more flexibility and potentially lower interest rates by considering the future value of your property after the ADU is built.

What is the interest rate for an ADU loan?

Interest rates for ADU loans vary based on several factors:

-

Credit Score: A higher credit score can help you secure a lower rate. Aim for a score above 720 for the best terms.

-

Loan Type: Fixed-rate loans offer stability, while adjustable-rate loans might start lower but can fluctuate.

-

Market Conditions: Economic factors like inflation or recession can influence rates. In times of low demand, rates might rise.

-

Lender Policies: Different lenders have varying risk assessments, so it’s wise to shop around.

Monitoring market trends and comparing offers can help you find the best rate for your ADU project.

Do you need 20% down for a construction loan?

The down payment requirement for a construction loan can vary. While some lenders may ask for 20%, others might accept less, especially if you have strong financial credentials.

Your loan-to-value (LTV) ratio plays a crucial role. A lower LTV ratio means you have more equity, which can reduce the down payment requirement. Additionally, some lenders offer flexible terms based on your credit score and financial stability.

It’s important to discuss options with multiple lenders to understand their specific requirements and find the best fit for your financial situation.

Understanding these key aspects of construction loans for ADUs can help you make informed decisions as you start on your ADU project. Next, we’ll dig into more detailed financing strategies and market insights.

Conclusion

Starting on an ADU project can be both exciting and daunting. The key to success lies in understanding the financing landscape and choosing the right strategy for your needs.

ADU Marketing Pros is here to guide you through this journey. Our expertise in marketing solutions for ADU construction and architecture firms is designed to help you stand out in a competitive market. We focus on showcasing your expertise rather than competing on price, ensuring you attract high-quality leads ready to invest in premium ADU projects.

When it comes to financing strategies, it’s crucial to evaluate all available options. Construction loans for ADUs might seem like a straightforward choice, but they come with complexities and higher costs. Alternatives like Home Equity Lines of Credit (HELOCs) and cash-out refinance options can offer more flexibility and potentially lower interest rates. These options consider the future value of your property, providing a more custom approach to financing your ADU.

Market insights are also vital. The demand for ADUs is growing, especially in areas like California, where zoning laws have become more favorable. This trend opens up opportunities for both rental income and increased property value. However, stay informed about market conditions and lending criteria, as these can impact your financing options and overall project success.

At ADU Marketing Pros, we understand the unique challenges faced by ADU businesses. Our custom digital marketing solutions, including targeted SEO and PPC strategies, are designed to help you steer these challenges and achieve measurable growth.

For more information on how we can support your ADU project, visit our services page. Let’s work together to make your ADU project a success!